Up next in 10

Professor AJ Kooti explains what is Journalizing in Accounting as part of his financial accounting course series.

Show More Show Less View Video Transcript

0:00

Alright, so we've talked about the T accounts, now we're going to talk about the other part to it

0:04

It's helper, if you will. The T accounts show us the calculations and what our balance is

0:11

What we're going to talk about now, which is journalizing, tells us the story of what happened

0:15

in those transactions. This is where the language of accounting comes into play. If it doesn't look

0:19

like this, then it's going to read differently. Think about a foreign language if you learned it

0:23

in high school. It's not going to make sense if it doesn't look like this, and what we really want

0:27

is to be able to make sense to the end user. We want to give them that story. So that's what we're

0:31

going to be doing in this one, which is journalizing and how to journalize or what are journal entries

0:36

A journal entry is a complete record of each transaction. So they're done one at a time and

0:41

they're done in a chronological order in one place. So it's just a long sheet that has all of

0:45

our debits and our credits in a journal entry form. Again, this is telling the story, not the

0:49

calculation side of it. The recording transactions in a journal is called journalizing. Again, real

0:55

real creative there, or what we call recognizing. So if you hear something or it asks you to recognize something

1:01

that is dealing with journalizing. Okay, I'm gonna show you an example

1:04

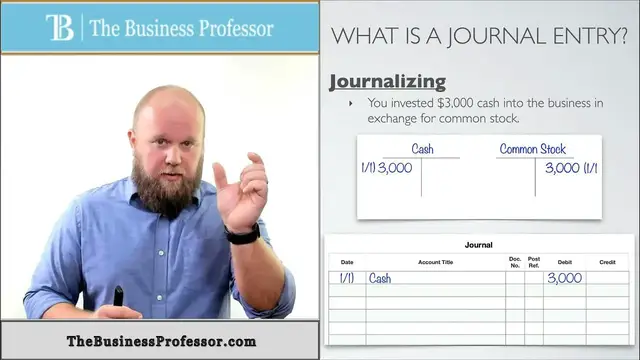

of what journal entries look like how they work So let use this as an example You invested cash into a business in exchange for common stock Now first and foremost I want you to understand this

1:17

and I think this is what makes accounting a little bit more tricky than other business classes or subjects, is that we're not a person here. When it says you, you're not doing this for you

1:26

We're doing this for the business. We're on the back end of the business. So this is kind of a new

1:30

way of thinking. You're going to have to put yourself in the business. So really, this is not saying that you invested in it. What we're doing this is as we, the business, have received $3,000

1:39

cash in exchange for common stock. And so let's look at what our T tables would look like here

1:46

So our T tables, one, cash, because our cash is changing. Ours, the business, is changing

1:52

So we're going to put cash. We're going to put our T table. There's our T table. And because our

1:56

cash is going up, we're going to put it on the debit side. Remember, cash is an asset. Debit

2:01

debit is plus side, so we're going to put it on the debit side, so we're going to put in there 1-1, I'm making up some date, and $3,000

2:07

That lets me know on a t-table format that my cash went up by $3,000

2:12

Then we also have the other side, because remember we have double entry accounting, something else has to happen

2:17

We have common stock Common stock remember is minus plus and our common stock in the business I know it says exchanging for common stock which alludes that we losing something But our common stock

2:28

the value of our business is actually going up. And so we're going to put on the plus side of

2:32

common stock. So if we did that, it's going to go there, 3,000, again, 1,1. Those match up

2:37

If we're looking at the accounting equation, cash is an asset. So we're saying our assets went up by

2:42

3,000. Common stock is an equity. So it's on the other side. It's on the claim side. So our claims

2:46

went at 3,000. So pretty much what we've done is we've said 3,000 equals 3,000 and that's true. So

2:51

at least we're following the accounting equation. But that's the t-tables. Now let's take a look at

2:55

what it would look like for a journal entry. Because again, this is the specifics. This is

2:59

how it has to look. This is where the structure comes into play. So this is what it looks like to

3:04

be a journal. We have different columns. We have dates. We have account titles. You have document

3:08

numbers. We're not going to use those. Post references. We're not going to use those. Those are more really in-depth accounting. I'm just getting you through the basics. And then we have

3:15

column that's specifically for debit and one specifically for credit. So first things first we're going to use our date. We want to go ahead and put a date to

3:22

this so we're gonna move the one one there and then always always always when

3:26

you journalizing you always start with the debit Whatever account is being debited For us the cash is being debited so we gonna move cash down we to put it all the way to the left side of that column And if we had other debits

3:39

we would continue following them along. We're also going to move our number that's under cash

3:43

into the debit column. So move the cash through 3,000 there. Again, that's one line of our debited

3:50

account. If we had more of them, we would continue doing this. Obviously, we would leave out the date

3:54

but the account title, we would just fall in line with that row. We would not move anything else

3:58

they'd all be in line. Okay. And then we'd keep putting the numbers in the debit. Once we're done

4:02

with all of our debits, then we move to the credits. And now we, in this situation, we only

4:06

have one credit. So what we're going to do is we're going to take that account title, put it right

4:10

under the debit, and I'm going to indent it just a little bit to show that it is a credit. So now

4:16

you can look at it specifically and it says, okay, cash is to the left. So that's debited. Common stock is to the right a little bit. That's it's credited. If it's both together, it's kind

4:24

of harder to see. And then I'm also going to put the $3,000 into the credit column. That is what a

4:29

journal entry looks like. You have at least one debit, at least one credit. The numbers are apart

4:36

so one's under the debit column, one's under the credit column. But that's how you deal with

4:40

journalizing entries. So you're going to see there's a whole lot more as we progress, but that's it

#Business Education

#Finance

#Accounting & Auditing

#Banking

#Investing

#Bookkeeping

#Debit & Checking Services