live_tv

Livestream Starting Soon

00

Hours

:

00

Minutes

:

00

Seconds

Up next in 10

#physicaltherapymedicare #occupationaltherapymedicare #speechtherapymedicare

✔️ If you would like to learn more about Medicare billing please join our FREE Facebook community at Medicare Billing for (Mostly) Cash Based PT, OT, SLP

✔️ If you are interested in learning more about billing Medicare check-out our website at Learn Medicare Billing

✔️ And if you just want to learn more about me 😀 check-out my Facebook profile.

If you would like to mail me:

Total Therapy Solutions

5900 Long Meadow Dr

Middletown, OH 45005

Show More Show Less View Video Transcript

0:00

Hi, and welcome. My name is Tony Maritato. I'm a licensed physical therapist. In today's

0:05

tutorial, I'm going to show you how to utilize the website ehealthinsurance.com to go ahead

0:11

and compare insurance policies available in your area to see if you might have a better

0:17

insurance policy option for you to determine the cost of your physical therapy services

0:22

So I'm going to go ahead and share my screen. This is a really informal class. So if you

0:27

guys have questions and watching this on the replay, go ahead and post your comments down below

0:32

And I'm more than happy to get to them. But this is the ehealthinsurance.com website. I have no

0:38

affiliation or connection to this website. This is simply the website that I use most frequently

0:43

You're going to see across the middle, there are a couple of tabs. There is a tab for Medicare

0:47

There's a tab for family, individual, small business, dental vision, and short-term

0:52

We're going to look at individuals and family. I'm going to put in the zip code

0:57

This is where I'm located here in Middletown, Ohio. I'm going to click find health insurance plans

1:03

It's going to ask for county. I'm going to leave it as Butler. We're going to go next

1:08

I'm only looking at affordable care plans. Next. I'm going to leave this information

1:15

I choose male or female. I chose male. The date of birth, no tobacco use

1:20

I'm not going to add any children or a spouse. So we'll go next

1:26

If you are living in a household with an income under $50,000 a year, there are some subsidies available

1:33

I'm going to leave that as no. And I'm just going to go to see the unsubsidized plans

1:40

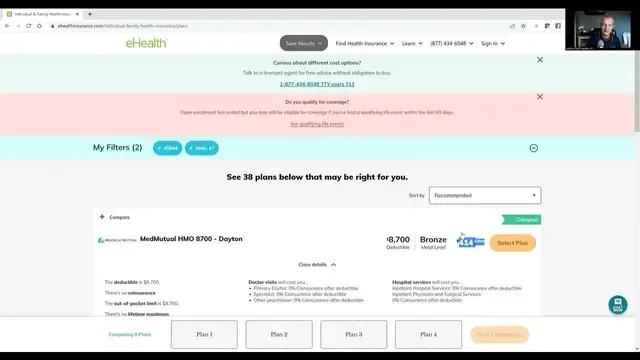

And so this is where we can start to see there's approximately 38 plans available

1:46

This is sorted by recommendation. So the first plan they recommend is a high deductible plan. It is a MedMutual HMO plan. It has an $8,700 deductible. A couple of the key things that you want to look at, and we'll talk about this terminology, the monthly premium for this plan is $414.12 per month

2:10

So the monthly premium is the amount that you pay, whether you use the insurance policy or not

2:16

It is the cost of having insurance. It does not get applied toward your deductible

2:21

It does not get applied toward any benefits. It is simply the amount you have to pay in order to have an eligible health insurance policy The deductible in this case is the amount that you will pay out of pocket

2:39

before the insurance coverage starts to kick in. So for example, if an individual has this policy with an $8,700 deductible

2:49

and it is January 1st, they've received no medical services in the calendar year

2:54

and the policy resets on January 1st when they go to their first doctor appointment

3:02

If you look down here, it says primary care doctor is 0% coinsurance after the deductible

3:09

has been met. So what would happen is the patient would go to the doctor on January 1st

3:15

They would receive a medical exam. Maybe that visit would be billed to the insurance company for a total bill rate of $375

3:24

But then based on the insurance contract between the provider and the insurance company, it will be readjusted down to perhaps $125

3:35

The difference between the total bill rate of $375 and the allowed amount of $125, that is considered a contract adjustment or a discount

3:44

That money is not owed to the provider or the insurance company

3:48

And what you, the patient, would be responsible for paying is the contracted allowed amount of $125

3:57

Once you make that payment to the doctor's office, the insurance company would also credit that payment automatically to your deductible

4:07

So your deductible would be reduced from $8,700. It would be reduced by $125

4:13

$5. Now, if that doctor referred you to physical therapy for shoulder pain or some other orthopedic

4:21

or neurologic condition, when you go to see that physical therapist, a similar thing would happen

4:26

You would receive an initial evaluation and treatment. That initial evaluation and treatment

4:32

might be billed at $320. And then the contracted allowed amount for that session might be $80

4:40

The $80 is owed to the physical therapy office. The $80 credit will be applied to the deductible

4:49

So now your deductible started at 8,700. It was reduced by the primary care allowed amount of 125 It also reduced by the physical therapy allowed amount of 80 And each medical service you receive will be contracted to the allowed amount

5:08

And then that allowed amount will reduce your deductible until you have paid a total of $8,700

5:16

Once you have met that deductible, once you've satisfied that deductible, Then, as you can see here, based on this plan, you will not pay anything for a primary care doctor visit. You will not pay anything for a specialist visit. Now, a specialist could be an orthopedic, it could be a physical therapist, occupational therapist, speech language pathologist, and for other practitioners, again, 0% coinsurance, you will not pay anything for those visits

5:45

If you look over here on the left side where I've highlighted, you can see other information. So generic drugs, $0 copay, preferred branded drugs, $0 coinsurance, non-branded specialty drugs

6:00

effectively once you pay the $8,700 for the calendar year all of the medical expenses as

6:07

long as they are deemed medically necessary will be covered and you can see here there is no lifetime

6:13

maximum with this particular plan so to compare this for a moment if we could review real quick

6:20

a monthly premium of $414 if I'm scrolling through other policies you can see that some of these this

6:30

one, for example, has a $6,000 deductible. It's a different insurance company. It has a $10 a month

6:38

more expensive monthly premium. So it goes up to $425. But you can also see down here

6:45

while the deductible is less, $2,700 less, primary care doctor has a $50 copay after the deductible

6:54

has been met for the first three visits. So even when you meet the $6,000 deductible, you'll still

7:01

have a $50 copay for the first three visits in the calendar year. Then it's a 35% coinsurance

7:07

After that, you can see for specialists, it's a 35% coinsurance. So using this as an example for

7:15

how much physical therapy might cost, if I had this policy, if I had satisfied my $6,000 deductible

7:22

When I go to a physical therapy visit if the bill rate is and the allowed amount is my responsibility would be 35 of the charge

7:37

Now, what's interesting about physical therapy is physical therapy is billed in 15-minute

7:42

units of time, depending on the procedure code you're receiving. So if you have manual therapy, therapeutic exercise, and therapeutic activity, and they

7:54

do a total of 60 minutes for those treatments, there's four units of therapy that have been

7:59

generated. Those are all direct one-to-one care interventions. You will be responsible in that case

8:07

for 35% of the insurance contract allowed amount. That would be paid by you to the physical therapy

8:14

department or office. And then the insurance would cover the other 65% of the allowed amount

8:21

And you can see here again, there is no lifetime maximum on a policy like this. The out-of-pocket maximum for this is $8,700. So as you're paying that 35% coinsurance, if you reach that $8,700 out-of-pocket max for the year, then the insurance would start to cover all of the expenses at 100% of the allowed amount

8:45

So guys, that is how you can compare insurance plans. And basically what you're looking at is trying to determine what is the coverage? What is the monthly premium? What do you expect as the potential patient you would be utilizing in a year

9:04

if you know that you're going to have a high utilization rate for a specific calendar year

9:10

you might want to look at a higher deductible that covers 100% of the expenses once that

9:16

deductible has been met, but a lower monthly premium, as opposed to a policy that has a higher

9:23

monthly premium, but that you have a lower out of pocket initially, simply because if you're going

9:32

to utilize a lot of medical expenses in the calendar year, it's better for you to save on

9:37

that monthly premium and pay at the time of service. So I hope this information was helpful

9:43

If you have more questions, absolutely. As I said, list them in the description of this video down

9:48

below, and I will catch you guys on the next tutorial. Thank you

#Health Insurance

#Health Education & Medical Training

#Physical Therapy

#Health Policy